What's new in MetaTrader 5

The history of updates of the desktop, mobile and web platforms

Terminal

- Added new API which enables request of MetaTrader 5 terminal data through applications using Python language.

Python is a modern high-level programming language for developing scripts and applications. It contains multiple libraries for machine learning, process automation, as well as data analysis and visualization.

MetaTrader package for Python is designed for efficient and fast obtaining of exchange data via interprocessor communication, directly from the MetaTrader 5 terminal. The data received via this pathway can be further used for statistical calculations and machine learning.

Connection

- Download the latest Python version at https://www.python.org/downloads/windows

- During Python installation, check "Add Python X.X to PATH%" to enable the launch of Python scripts from the command line.

- Install the MetaTrader 5 module from the command line

pip install MetaTrader5

- Add matplotlib and pytz packages

pip install matplotlib

pip install pytz

Functions

- MT5Initialize establishes connection with the MetaTrader 5 terminal

- MT5Shutdown closes the previously established connection to the MetaTrader 5 terminal

- MT5TerminalInfo receives status and parameters of the connected MetaTrader 5 terminal

- MT5Version returns the MetaTrader 5 terminal version

- MT5WaitForTerminal waits till the MetaTrader 5 terminal connects to the trade server

- MT5CopyRatesFrom receives bars from the MetaTrader 5 terminal starting from the specified date

- MT5CopyRatesFromPos receives bars from the MetaTrader 5 terminal starting from the specified index

- MT5CopyRatesRange receives bars in the specified date range from the MetaTrader 5 terminal

- MT5CopyTicksFrom receives ticks from the MetaTrader 5 terminal starting from the specified date

- MT5CopyTicksRange receives ticks for the specified date range from the MetaTrader 5 terminal

- The Market and Signal sections have been optimized. Now the product and signal showcases run up to seven times faster and thus provide a better service browsing experience.

- Added support for "Market", "Signals" and "Search" in Wine. Linux and Mac OS users can now access the largest store of trading applications along with the copy trading service.

- The built-in learning program has been translated into more than 30 languages, including Spanish, Chinese, Portuguese and German, among others. To view interactive tips in the desired language, switch to the required interface language using the View menu.

- New options enable verification of phone numbers and emails, which are specified by traders when opening demo and preliminary accounts.

The need for data verification is determined by the broker. If the option is enabled, confirmation codes are automatically sent to the trader during an account request and special code fields appear in the dialog box:

Confirmation codes are valid for several minutes. If the code is not entered in the field within this time frame, the trader will need to repeat the procedure.

Before sending codes, the system checks whether the specified phone/email was previously confirmed. If the trader has already passed verification from his or her computer, an account will be opened without additional confirmation. Thus, there will be no additional burden for traders during an account request.

- MQL5.community payment options through the PayPal system have been expanded. Purchases can now be performed with one click, using this system.

How it works

After you log in using your PayPal account when making a purchase, you will be requested to allow further payments to our company:

By confirming this option, and you will be able to perform further purchases with one click, by pressing the previously saved account button:

If you click "Cancel and return to MetaQuotes Software Corp.", you will make the payments in a normal way, by entering the PayPal account details manually, for each purchase.

The MQL5.com website and the MetaTrader 5 platform do not store your payment details. When you deposit funds, make a purchase in the Market service or subscribe to a Signal, the data verification is performed on the payment system side.

You can always remove your PayPal account link.

- Strategy Tester improvements and optimization.

We have introduced a large number of hidden improvements and fixed errors to optimize the Strategy Tester operation. The update enables much faster testing for some of the task types and higher operation stability. Major improvements include:

Operations with frames

Operations with frames on local, network and cloud agents have been optimized. Such operations are now processed faster and are never skipped.

Distribution of tasks to agents

The tester can now redistribute tasks to agents during the optimization process. If a new agent has become available (or one of the previously used ones has been released), the tester automatically creates a new package of tasks, using those which were earlier distributed among other agents. Tasks can also be redistributed if slow agents are detected. Tasks of such agents are sent to other agents to complete the optimization faster.

Task distribution in math calculation mode has become much faster.

Optimization statistics in the Journal

Optimization logging has been extended: it includes detailed statistics related to the MQL5 Cloud Network usage and to the enabling and disabling of cloud agents, among others.

Operation in full optimization log mode

For optimal resource consumption, not all messages from agents are recorded to the tester log. To view all logs, you can enable the "Full optimization logs" option using the tester log context menu. Previously, this mode significantly slowed the optimization process. Now the calculation time is not affected.

MQL5 Cloud Network

Optimized operation of cloud testing agents. Now computation tasks are distributed more efficiently.

- The built-in calendar features publications of more than 900 indicators related to the 18 largest global economies, including US, European Union, Japan and the UK, among others. Relevant data is collected from open sources in real time. By regularly checking the service, traders remain informed on the latest global news and can take informed trading decisions.

The economic calendar is available in desktop terminals and websites, as well as on mobile devices. The application can be opened using the Calendar context menu in the terminal:

Select your platform and download the Tradays apps:

In addition to calendar functions available in the desktop platform, the mobile version provides event reminders and access to a complete history of indicators in the form of charts and tables.

- Added automatic generation of custom symbol bar history during import of tick history. Now, if tick data of a custom symbol changes, corresponding bars are automatically recalculated:

- Thus, unified data is preserved in the platform.

- After importing tick data (provided that there is enough data), there is no need to import bars since they are automatically calculated by the terminal.

Changes concern the import of ticks performed via the terminal interface, as well as the update of ticks performed from MQL5 applications using the CustomTicks* function. Any changes in tick data lead to recalculation of the corresponding 1-minute bars of the custom symbol.

- Fixed data update in the Data Window when using a crosshair on a detached chart.

- Fixed tick history saving. In earlier versions, multiple ticks within a millisecond could be saved in the wrong order.

- Fixed generation of charts based on a too short price history (less than a day) available on the server.

MQL5

- Added MQL5 service debugging option. These applications can now be tested similar to Expert Advisors and indicators.

- New profit and margin calculation modes have been added in the ENUM_SYMBOL_CALC_MODE enumeration:

- SYMBOL_CALC_MODE_EXCH_BONDS — calculation for exchange bonds.

- SYMBOL_CALC_MODE_EXCH_STOCKS_MOEX — calculation for the stocks traded on the Moscow Exchange.

- SYMBOL_CALC_MODE_EXCH_BONDS_MOEX — calculation for the bonds traded on the Moscow Exchange.

- SYMBOL_CALC_MODE_EXCH_BONDS — calculation for exchange bonds.

- The new TesterDeposit function enables the emulation of deposit operations during testing. The function can be useful when testing money management strategies.

bool TesterDeposit( double money // the deposit amount );

- During the OnDeinit method execution, the MQL5 application does not receive any events from the terminal. Previously, applications occasionally failed to complete de-initialization (for example, to delete all created objects) due to the receiving of other events.

- Fixed occasional errors which could occur after a change in the custom symbol tick history for the current day.

- Fixed occasional application slowdown when using a large number (tens of thousands) of graphical objects.

- Fixed terminal freezing in the case of frequent trading history calls from MQL5 programs.

- Fixed iBarShift function operation. With the "exact=false" flag and request outside the data, the function returned the oldest bar number instead of the newest one.

Tester

- Fixed determination of the cores number on computers with processors having several NUMA nodes.

- Added possibility to run testing and optimization with the zero initial deposit, since deposit operations can be emulated during testing using the new TesterDeposit function.

MetaEditor

- The code styler command can now be added to the toolbar for quick access.

- Fixed switching to parameter definition and viewing of related data when using non-Unicode characters in function and variable names.

Documentation has been updated.

The update is available through the LiveUpdate system.

Terminal

- Completely revised built-in Economic Calendar.

The Economic Calendar is our proprietary solution. Therein you will find over 600 financial news and indicators related to the 13 largest global economies: USA, European Union, Japan, UK, Canada, Australia, China among others. Relevant data is collected from open sources in real time.

The new version features updated contents and advanced event filters: by time, priority, currencies and countries.

The calendar data can now be accessed from MQL5 programs. Please see below for details.

- Added new type of MQL5 applications — Services. This new type enables the creation of custom price feeds for the terminal, i.e. to implement price delivery from external systems in real time, just like it is implemented on brokers' trade servers.

Unlike Expert Advisors, indicators and scripts, services are not linked to a specific chart. Such applications run in the background and are launched automatically when the terminal is started (unless such an app was forcibly stopped).

Services can be managed from a new section within the Navigator window:

How to create services

To create a service template, use the corresponding MQL5 Wizard option. Services have one OnStart entry point, similar to scripts. At this point, you can implement an endless data receiving and handling cycle using network functions.

How to launch services

To run multiple Expert Advisor or indicator copies with different parameters, you should launch them on different charts. In this case different program instances are created, which then operate independently. Services are not linked to charts, therefore a special mechanism has been implemented for the creation of service instances.

Select a service from the Navigator and click "Add service" in its context menu. This will open a standard MQL5 program dialog, in which you can enable/disable trading and access to signal settings, as well as set various parameters.

A service instance can be launched and stopped using the appropriate instance menu. To manage all instances, use the service menu.

- A learning program has been added.

The new feature will help beginners in learning how to interact with the platform. We have added over 100 interactive tips concerning the main platform features.

- Tips are seamlessly displayed as a progress bar on the toolbar and thus they do not distract the user.

- Tips only appear for the actions which you have never performed in the platform.

- All tips include interactive links, by which you can navigate to the relevant interface elements. For example, a trading dialog or a menu with the desired program can be launched straight from the tip.

- The trading account history can be presented as positions. The platform collects data on deals related to the position (opening, volume increase, partial or full closing) and groups the information into a single record. Thus you can access position details: open and close time, volume, price and result. This efficient presentation form is now available in history reports exported to files.

- Added new API enabling request of MetaTrader 5 terminal data through applications using the R language.

We have prepared a special MetaTrader package. It contains DLL for interactions between R and the MetaTrader 5 terminal, documentation and auxiliary r files. We are completing the package registration in the CRAN repository, after which it will be available for download and installation.

The package can be installed using a special command:

R CMD INSTALL --build MetaTrader

The following commands related to data request are available:

- MT5Initialize initializes and establishes connection with the MetaTrader 5 terminal. If necessary, the terminal is launched during command execution.

- MT5Shutdown de-initializes and disconnects from MetaTrader 5.

- MT5Version gets the MetaTrader 5 terminal version.

- MT5TerminalInfo gets the state and parameters of terminal connection to a broker's server (account number and server address).

- MT5WaitTerminal waits for the MetaTrader 5 terminal to connect to a broker's server.

- MT5CopyTicksFrom(symbol, from, count, flags) copies the specified number of ticks starting from the specified date. The date is specified in milliseconds since 01.01.1970.

- MT5CopyTicksRange(symbol, from, to, flags) copies ticks from within the specified period. The dates are specified in milliseconds since 01.01.1970.

- MT5CopyRatesFrom(symbol, timeframe, from, count) copies the specified number of one-minute bars starting from the specified date. The date is specified in seconds since 01.01.1970.

- MT5CopyRatesFromPos(symbol, timeframe, start_pos, count) copies one-minute bars from the specified position relative to the last bar.

- MT5CopyRatesFromRange(symbol, timeframe, date_from, date_to) copies bars from within the specified period. The dates are specified in seconds since 01.01.1970.

The list of supported commands will be further expanded.

- Optimized Close By dialog used for closing a position by an opposite one. Now, the dialog is not slowed down even if you have a large number of open positions.

- Fixed synthetic symbol calculation errors, due to which data could be occasionally skipped.

- When a custom symbol is deleted, files storing its tick and bar history are also deleted. This avoids the accumulation of unused data on the hard disk.

- Fixed display of search results on High DPI screens.

MQL5

- Implemented access to economic calendar data from MQL5 programs.

New functions

CalendarCountryById — gets country description by identifier.bool CalendarCountryById( const long country_id, // country ID MqlCalendarCountry& country // country description );

CalendarEventById — gets event description by identifier.bool CalendarEventById( const long event_id, // event ID MqlCalendarEvent& event // event description );

CalendarValueById — gets event value description by identifier.bool CalendarValueById( const long value_id, // value ID MqlCalendarValue& value // value description );

CalendarEventByCountry — gets the array of available events for the country.bool CalendarEventByCountry( string country_code, // country code MqlCalendarEvent& events[] // array of events );

CalendarEventByCurrency — gets the array of available events for the affected currency.bool CalendarEventByCurrency( string currency, // currency MqlCalendarEvent& events[] // array of events );

CalendarValueHistoryByEvent — gets the array of values for the specified time period, by event identifier.bool CalendarValueHistoryByEvent( ulong event_id, // event ID MqlCalendarValue& values[], // array of values datetime datetime_from, // period beginning date datetime datetime_to=0 // period end date );

CalendarValueHistory — gets the array of values for the specified time period for all events, filtered by country and/or currency.bool CalendarValueHistory( MqlCalendarValue& values[], // array of values datetime datetime_from, // beginning of period datetime datetime_to=0, // end of period string country_code=NULL, // country code string currency=NULL // currency );

CalendarValueLastByEvent — gets an array of last event values by identifier. This function enables the request of the values which have appeared since the previous request. The in/out parameter "change_id" is additionally used for this operation.

Every time the calendar database changes, the "change_id" property (the last change identifier) is updated. During data request, you specify "change_id" and the terminal returns events which appeared after that time, as well as the current "change_id" value, which can be used for the next request. During the first function call, specify the zero "change_id": the function will not return any events, but will return the current "change_id" for further requests.bool CalendarValueHistory( ulong event_id, // event ID ulong& change_id, // last calendar change ID MqlCalendarValue& values[] // array of values );

CalendarValueLast — gets the array of last values for all events, filtered by country and/or currency. This function enables the request of the values which have appeared since the previous request. Similarly to CalendarValueLastByEvent, the "change_id" property is used for the request.bool CalendarValueHistory( ulong event_id, // event ID ulong& change_id, // last calendar change ID MqlCalendarValue& values[], // array of values string country_code=NULL, // country code string currency=NULL // currency );

New structures

MqlCalendarCountry — country description.struct MqlCalendarCountry { ulong id; // country ID in ISO 3166-1 string name; // text name of the country string code; // code name of the country in ISO 3166-1 alpha-2 string currency; // country currency code string currency_symbol; // country currency symbol/sign string url_name; // country name used in URL on mql5.com };

MqlCalendarEvent — event description.struct MqlCalendarEvent { ulong id; // event ID ENUM_CALENDAR_EVENT_TYPE type; // event type ENUM_CALENDAR_EVENT_SECTOR sector; // sector to which the event belongs ENUM_CALENDAR_EVENT_FREQUENCY frequency; // event release frequency ENUM_CALENDAR_EVENT_TIMEMODE time_mode; // event release time mode ulong country_id; // country ID ENUM_CALENDAR_EVENT_UNIT unit; // unit for the event values ENUM_CALENDAR_EVENT_IMPORTANCE importance; // event importance ENUM_CALENDAR_EVENT_MULTIPLIER multiplier; // event importance multiplier uint digits; // number of decimal places in the event value string source_url; // source URL string event_code; // event code string name; // text name of the event in the terminal language };

MqlCalendarValue — event value description.struct MqlCalendarValue { ulong id; // value ID ulong event_id; // event ID datetime time; // event date and time datetime period; // period, for which the event is published int revision; // published indicator revision in relation to the reported period long actual_value; // current event value long prev_value; // previous event value long revised_prev_value; // revised previous event value long forecast_value; // forecast event value ENUM_CALENDAR_EVENT_IMPACRT impact_type; // potential impact on the currency rate };

New enumerationsenum ENUM_CALENDAR_EVENT_FREQUENCY { CALENDAR_FREQUENCY_NONE =0, // not used CALENDAR_FREQUENCY_WEEK =1, // weekly CALENDAR_FREQUENCY_MONTH =2, // monthly CALENDAR_FREQUENCY_QUARTER =3, // quarterly CALENDAR_FREQUENCY_YEAR =4, // yearly CALENDAR_FREQUENCY_DAY =5, // daily }; enum ENUM_CALENDAR_EVENT_TYPE { CALENDAR_TYPE_EVENT =0, // event (meeting, speech, etc.) CALENDAR_TYPE_INDICATOR =1, // indicator CALENDAR_TYPE_HOLIDAY =2, // holiday }; enum ENUM_CALENDAR_EVENT_SECTOR { CALENDAR_SECTOR_NONE =0, // no CALENDAR_SECTOR_MARKET =1, // market CALENDAR_SECTOR_GDP =2, // GDP CALENDAR_SECTOR_JOBS =3, // jobs CALENDAR_SECTOR_PRICES =4, // prices CALENDAR_SECTOR_MONEY =5, // money CALENDAR_SECTOR_TRADE =6, // trade CALENDAR_SECTOR_GOVERNMENT =7, // government CALENDAR_SECTOR_BUSINESS =8, // business CALENDAR_SECTOR_CONSUMER =9, // consumer CALENDAR_SECTOR_HOUSING =10, // housing CALENDAR_SECTOR_TAXES =11, // taxes CALENDAR_SECTOR_HOLIDAYS =12, // holidays }; enum ENUM_CALENDAR_EVENT_IMPORTANCE { CALENDAR_IMPORTANCE_NONE =0, // no CALENDAR_IMPORTANCE_LOW =1, // low CALENDAR_IMPORTANCE_MODERATE =2, // moderate CALENDAR_IMPORTANCE_HIGH =3, // high }; enum ENUM_CALENDAR_EVENT_UNIT { CALENDAR_UNIT_NONE =0, // no CALENDAR_UNIT_PERCENT =1, // percent CALENDAR_UNIT_CURRENCY =2, // national currency CALENDAR_UNIT_HOUR =3, // number of hours CALENDAR_UNIT_JOB =4, // number of jobs CALENDAR_UNIT_RIG =5, // number of rigs CALENDAR_UNIT_USD =6, // US dollar CALENDAR_UNIT_PEOPLE =7, // number of people CALENDAR_UNIT_MORTGAGE =8, // number of mortgages CALENDAR_UNIT_VOTE =9, // number of votes CALENDAR_UNIT_BARREL =10, // number of barrels CALENDAR_UNIT_CUBICFEET =11, // volume in cubic feet CALENDAR_UNIT_POSITION =12, // number of job positions CALENDAR_UNIT_BUILDING =13 // number of buildings }; enum ENUM_CALENDAR_EVENT_MULTIPLIER { CALENDAR_MULTIPLIER_NONE =0, // no CALENDAR_MULTIPLIER_THOUSANDS =1, // thousands CALENDAR_MULTIPLIER_MILLIONS =2, // millions CALENDAR_MULTIPLIER_BILLIONS =3, // billions CALENDAR_MULTIPLIER_TRILLIONS =4, // trillions }; enum ENUM_CALENDAR_EVENT_IMPACRT { CALENDAR_IMPACT_NA =0, // not available CALENDAR_IMPACT_POSITIVE =1, // positive CALENDAR_IMPACT_NEGATIVE =2, // negative }; enum ENUM_CALENDAR_EVENT_TIMEMODE { CALENDAR_TIMEMODE_DATETIME =0, // the source publishes the exact time CALENDAR_TIMEMODE_DATE =1, // the event takes the whole day CALENDAR_TIMEMODE_NOTIME =2, // the source does not publish the event time CALENDAR_TIMEMODE_TENTATIVE =3, // the source provides only date, but does not publish the exact time in advance, exact time is added when event occurs };

New error codesERR_CALENDAR_MORE_DATA =5400, // the array is too small for the whole result (values which fit in the array were passed) ERR_CALENDAR_TIMEOUT =5401, // timed out waiting for a response to the calendar data request ERR_CALENDAR_NO_DATA =5402, // data not found

- Fixes and operation speed improvements related to tick and bar history.

- Fixes and significant operation speed improvements related to tick and bars history modification functions of custom trading symbols, CustomTicks* and CustomRates*.

- New data conversion functions.

CharArrayToStruct copies a uchar array to a POD structure.

bool CharArrayToStruct( void& struct_object, // structure const uchar& char_array[], // array uint start_pos=0 // starting position in the array );

StructToCharArray copies a POD structure to a uchar array.

bool StructToCharArray( const void& struct_object, // structure uchar& char_array[], // array uint start_pos=0 // starting position in the array );

- Added MathSwap function for changing byte order in ushort, uint and ulong values.

ushort MathSwap(ushort value); uint MathSwap(uint value); ulong MathSwap(ulong value);

- Added network functions for creating TCP connections to remote hosts via system sockets:

- SocketCreate creates a socket with specified flags and returns its handle

- SocketClose closes the socket

- SocketConnect connects to the server, with timeout control

- SocketIsConnected checks if the socket is currently connected

- SocketIsReadable gets the number of bytes which can be read from the socket

- SocketIsWritable checks if data writing to this socket is possible at the current time

- SocketTimeouts sets data receiving and sending timeouts for the system socket object

- SocketRead reads data from a socket

- SocketSend writes data to a socket

- SocketTlsHandshake initiates a secure TLS (SSL) connection with the specified host using the TLS Handshake protocol

- SocketTlsCertificate receives information concerning the certificate used for secure network connection

- SocketTlsRead reads data from a secure TLS connection

- SocketTlsReadAvailable reads all available data from a secure TLS connection

- SocketTlsSend sends data using a secure TLS connection

The address of the host, to which connection using network functions is established, must be explicitly added to the list of allowed addresses in terminal settings.

New error codes have been added for operations with network functions:

- ERR_NETSOCKET_INVALIDHANDLE (5270): invalid socket handle passed to the function

- ERR_NETSOCKET_TOO_MANY_OPENED (5271): too many sockets open (maximum 128)

- ERR_NETSOCKET_CANNOT_CONNECT (5272): error while connecting to remote host

- ERR_NETSOCKET_IO_ERROR (5273): error while sending/receiving data from the socket

- ERR_NETSOCKET_HANDSHAKE_FAILED (5274): secure connection establishment error (TLS Handshake)

- ERR_NETSOCKET_NO_CERTIFICATE (5275) — no data about certificate used for secure connection

- Added new functions for string operations:

StringReserve reserves for a string the memory buffer of the specified size.

bool StringReserve( string& string_var, // string uint new_capacity // buffer size for the string );

StringSetLength sets the specified string length in characters.

bool StringSetLength( string& string_var, // string uint new_length // new string length );

- Added new function for array operations:

ArrayRemove removes from an array the specified number of elements starting with the specified index.

bool ArrayRemove( void& array[], // array of any type uint start, // the index to start removal uint count=WHOLE_ARRAY // number of elements );

ArrayInsert inserts to a receiver array the specified number of elements from the source array, starting with the specified index.

bool ArrayInsert( void& dst_array[], // receiver array const void& src_array[], // source array uint dst_start, // index in the receiver array where to insert uint src_start=0, // index in the source array to start copying uint count=WHOLE_ARRAY // number of inserted elements );

ArrayReverse reverses in an array the specified number of elements starting with the specified index.

bool ArrayReverse( void& array[], // array of any type uint start=0, // index to start reversing uint count=WHOLE_ARRAY // number of elements );

- New "uint count" parameter has been added in functions CustomRatesUpdate, CustomRatesReplace, CustomTicksAdd and CustomTicksReplace. It allows specification of the number of elements of the passed array, which will be used for these functions. The WHOLE_ARRAY value is used for the parameter by default. It means that the whole array will be utilized.

- Added CustomBookAdd function to pass the status of the Depth of Market for a custom symbol. The function allows broadcasting the Depth of Market as if the prices arrive from a broker's server.

int CustomBookAdd( const string symbol, // symbol name const MqlBookInfo& books[] // an array with the DOM elements descriptions uint count=WHOLE_ARRAY // number of elements to be used );

- Added CustomSymbolCreate function overloading. This allows the creation of a custom trading symbol based on an existing one. After creation, any symbol property can be edited using corresponding functions.

bool CustomSymbolCreate( const string symbol_name, // custom symbol name const string symbol_path="", // name of the group in which the symbol will be created const string symbol_origin=NULL // name of the symbol based on which the custom symbol will be created );

The name of the symbol, from which the properties of for the custom symbol should be copied, is specified in the "symbol_origin" parameter.

- The StringToTime function converting the string with date/time to a datetime value has been updated. Now it supports the following date formats:

- yyyy.mm.dd [hh:mi]

- yyyy.mm.dd [hh:mi:ss]

- yyyymmdd [hh:mi:ss]

- yyyymmdd [hhmiss]

- yyyy/mm/dd [hh:mi:ss]

- yyyy-mm-dd [hh:mi:ss]

- New TERMINAL_VPS property in the ENUM_TERMINAL_INFO_INTEGER enumeration; it shows that the terminal is running on the MetaTrader Virtual Hosting server (MetaTrader VPS). If an application is running on a hosting server, you can disable all its visual functions, since the virtual server does not have a graphical user interface.

- New SYMBOL_EXIST property in the ENUM_SYMBOL_INFO_INTEGER enumeration, means that the symbol under this name exists.

- Fixed typing when using template function pre-declarations.

- Added re-initialization of indicators when changing a trading account.

- Optimized StringSplit function.

- Fixed errors in the standard library operation.

Tester

- Added TesterStop function — routine early shutdown of an Expert Advisor on a test agent. Now you can forcibly stop testing after reaching the specified number of losing trades, a preset drawdown level or any other criterion.

Testing completed using this function is considered successful. After the function call, the trading history obtained during testing and all trade statistics are passed to the terminal.

- Disabled ability to test and optimize Expert Advisors through MQL5 Cloud Network in the real tick mode. This mode can only be used on local agents and local network farms.

- Improved work with indicators during visual testing. Now the price chart and indicator lines are drawn synchronously, even for the maximum visualization speed.

- Optimized and significantly accelerated testing and optimization.

- Fixed debugging of indicators on historical data. Now the OnInit and OnDeinit indicator functions can be properly debugged.

- Implemented faster access to historical data when testing multicurrency Expert Advisors.

- Fixed occasional freezing of the visual tester during debugging on historical data.

- Implemented faster start of optimization passes when processing a task package by an agent.

- Changed policy of distributing task packages to testing agents. The package size has been increased and thus resource consumption on network operations has been significantly reduced.

- Changed behavior of options enabling the use of local, network and cloud agents. Now, when you switch off the options, the agents complete processing of received tasks, while no more new tasks are given to them. In earlier versions, the behavior was similar to the "Disable" command, which immediately stopped agent operation.

MetaEditor

- Added support for non-ANSI characters in the debugger. Now, the expressions are properly displayed even if the variable name is specified in Cyrillic.

- Fixed display of search results on High DPI screens.

Added user interface translation into Croatian.

Documentation has been updated.

Terminal

- Now you can detach financial symbol charts from the trading terminal window.

This feature is convenient when using multiple monitors. Thus, you may set the main platform window on one monitor to control your account state, and move your charts to the second screen to observe the market situation. To detach a chart from the terminal, disable the Docked option in its context menu. After that, move the chart to the desired monitor.

A separate toolbar on detached charts allows applying analytical objects and indicators without having to switch between monitors. Use the toolbar context menu to manage the set of available commands or to hide it.

- Fully updated the built-in chats. Now they support group

dialogs and channels. Conduct private discussions with a group of

people in a unified environment without switching between different

dialogs and create channels according to your interests and languages.

Communicate with colleagues and friends at MQL5.community without

visiting the website.

Group chats and channels can be public or private. Their creators decide whether it is possible to join them freely or only by invitation. You can also assign moderators to channels and chats for additional communication control.

- Added support for extended volume accuracy for

cryptocurrency trading. Now the minimum possible volume of trading

operations is 0.00000001 lots. The market depth, the time and sales, as

well as other interface elements now feature the ability to display

volumes accurate to 8 decimal places.

The minimal volume and its change step depend on financial instrument settings on the broker's side.

- Added the tab of articles published on MQL5.community

to the Toolbox window. Over 600 detailed materials on the development

of trading strategies in MQL5 are now available directly in the

terminal. New articles are published every week.

- Added support for extended authentication using certificates when working under Wine.

- Fixed display of the market depth when it is limited to one level.

- Added the "Save As Picture" command to the Standard

toolbar. Now, it is much easier to take pictures of charts and share

them in the community.

- Fixed applying the time shift when importing bars and ticks. Previously, the shift was not applied in some cases.

- Fixed terminal freezing in case of a large amount of economic calendar news.

MQL5

- Added native support for .NET libraries with "smart"

functions import. Now .NET libraries can be used without writing special

wrappers — MetaEditor does it on its own.

To work with .NET library functions, simply import DLL itself without defining specific functions. MetaEditor automatically imports all functions it is possible to work with:

- Simple structures (POD, plain old data) — structures that contain only simple data types.

- Public static functions having parameters, in which only simple types and POD structures or their arrays are used

To call functions from the library, simply import it:

#import "TestLib.dll" //+------------------------------------------------------------------+ //| Script program start function | //+------------------------------------------------------------------+ void OnStart() { int x=41; TestClass::Inc(x); Print(x); }

The C# code of the Inc function of the TestClass looks as follows:

public class TestClass { public static void Inc(ref int x) { x++; } }

As a result of execution, the script returns the value of 42.

The work on support for .NET libraries continues. Their features are to be expanded in the future.

- Added support for working with WinAPI functions to Standard

Library. Now, there is no need to import libraries manually and describe

function signatures to use operating system functions in an MQL5

program. Simply include the header file from the MQL5\Include\WinAPI

directory.

WinAPI functions are grouped in separate files by their purpose:

- libloaderapi.mqh — working with resources

- memoryapi.mqh — working with memory

- processenv.mqh — working with environment

- processthreadsapi.mqh — working with processes

- securitybaseapi.mqh — working with OS security system

- sysinfoapi.mqh — obtaining system information

- winbase.mqh — common functions

- windef.mqh — constants, structures and enumerations

- wingdi.mqh — working with graphical objects

- winnt.mqh — working with exceptions

- winreg.mqh — working with the registry

- winuser.mqh — working with windows and interface

- errhandlingapi.mqh — handling errors

- fileapi.mqh — working with files

- handleapi.mqh — working with handles

- winapi.mqh — including all functions (WinAPI header files)

The binding works only with the 64-bit architecture.

- libloaderapi.mqh — working with resources

- Added support for the inline, __inline and __forceinline

specifiers when parsing code. The presence of the specifiers in the code

causes no errors and does not affect the compilation. At the moment,

this feature simplifies transferring С++ code to MQL5.

Find more information about specifiers in MSDN.

- Significantly optimized execution of MQL5 programs. In some

cases, the performance improvement can reach 10%. Recompile your

programs in the new MetaEditor version to make them run faster.

Unfortunately, new programs will not be compatible with previous terminal versions due to this additional optimization. Programs compiled in MetaEditor version 1912 and later cannot be launched in terminal versions below 1912. Programs compiled in earlier MetaEditor versions can run in new terminals.

- Significantly optimized multiple MQL5 functions.

- Added new properties for attaching/detaching charts from the terminal main window and managing their position.

Added the following properties to the ENUM_CHART_PROPERTY_INTEGER enumeration:

- CHART_IS_DOCKED — the chart window is docked. If set to 'false', the chart can be dragged outside the terminal area.

- CHART_FLOAT_LEFT — the left coordinate of the undocked chart window relative to the virtual screen.

- CHART_FLOAT_TOP — the upper coordinate of the undocked chart window relative to the virtual screen.

- CHART_FLOAT_RIGHT — the right coordinate of the undocked chart window relative to the virtual screen.

- CHART_FLOAT_BOTTOM — the bottom coordinate of the undocked chart window relative to the virtual screen.

Added the following functions to the ENUM_TERMINAL_INFO_INTEGER enumeration:

- TERMINAL_SCREEN_LEFT — the left coordinate of the virtual screen. A virtual screen is a rectangle that covers all monitors. If the system has two monitors ordered from right to left, then the left coordinate of the virtual screen can be on the border of two monitors.

- TERMINAL_SCREEN_TOP — the top coordinate of the virtual screen.

- TERMINAL_SCREEN_WIDTH — terminal width.

- TERMINAL_SCREEN_HEIGHT — terminal height.

- TERMINAL_LEFT — the left coordinate of the terminal relative to the virtual screen.

- TERMINAL_TOP — the top coordinate of the terminal relative to the virtual screen.

- TERMINAL_RIGHT — the right coordinate of the terminal relative to the virtual screen.

- TERMINAL_BOTTOM — the bottom coordinate of the terminal relative to the virtual screen.

- Added the volume_real field to the MqlTick and MqlBookInfo

structures. It is designed to work with extended accuracy volumes. The

volume_real value has a higher priority than 'volume'. The server will

use this value, if specified.

struct MqlTick

{

datetime time; // Last price update time

double bid; // Current Bid price

double ask; // Current Ask price

double last; // Current price of the Last trade

ulong volume; // Volume for the current Last price

long time_msc; // Last price update time in milliseconds

uint flags; // Tick flags

double volume_real; // Volume for the current Last price with greater accuracy

};struct MqlBookInfo { ENUM_BOOK_TYPE type; // order type from the ENUM_BOOK_TYPE enumeration double price; // price long volume; // volume double volume_real; // volume with greater accuracy };

- Added new properties to the ENUM_SYMBOL_INFO_DOUBLE enumeration:

- SYMBOL_VOLUME_REAL — the volume of the last executed deal;

- SYMBOL_VOLUMEHIGH_REAL — the highest deal volume for the current day;

- SYMBOL_VOLUMELOW_REAL — the lowest deal volume for the current day.

Use the SymbolInfoDouble function to get these properties.

- SYMBOL_VOLUME_REAL — the volume of the last executed deal;

- Added the MQL_FORWARD property to the ENUM_MQL_INFO_INTEGER enumeration — forward test mode flag.

- Added the pack( integer_value ) property for structures. It

allows you to set the alignment of the fields arrangement within a

structure, which can be necessary when working with DLL. The values of

1, 2 ,4 ,8 and 16 are possible for integer_value.

If the property is not defined, the default alignment of 1 byte is used — pack(1).

Example of use:

//+------------------------------------------------------------------+ //| Default packing | //+------------------------------------------------------------------+ struct A { char a; int b; }; //+------------------------------------------------------------------+ //| Specified packing | //+------------------------------------------------------------------+ struct B pack(4) { char a; int b; }; //+------------------------------------------------------------------+ //| Script program start function | //+------------------------------------------------------------------+ void OnStart() { Print("sizeof(A)=",sizeof(A)); Print("sizeof(B)=",sizeof(B)); } //+------------------------------------------------------------------+

Conclusion:

sizeof(A)=5 sizeof(B)=8

Find more information about alignment within structures in MSDN.

- Relaxed requirements for casting enumerations. In case of an

implicit casting, the compiler automatically substitutes the value of a

correct enumeration and displays a warning.

For the following code:

enum Main { PRICE_CLOSE_, PRICE_OPEN_ }; input Main Inp=PRICE_CLOSE; //+------------------------------------------------------------------+ //| Start function | //+------------------------------------------------------------------+ void OnStart() { }

The compiler displays the warning:

implicit conversion from 'enum ENUM_APPLIED_PRICE' to 'enum Main'Previously, the following error was generated in that case:

'Main::PRICE_OPEN_' instead of 'ENUM_APPLIED_PRICE::PRICE_CLOSE' will be used

'PRICE_CLOSE' - cannot convert enumThe compiler will still display the error if enumerations are used incorrectly in the function parameters.

- Fixed compilation of template functions. Now, when using

overloaded template functions, only the necessary overload, rather than

all existing ones, is instantiated.

class X { }; void f(int) { } template<typename T> void a(T*) { new T(2); } // previously, the compiler generated the error here template<typename T> void a() { f(0); } void OnInit() { a<X>(); }

- Optimized some cases of accessing tick history via the CopyTicks* functions.

- Added the new TesterStop function allowing for early

completion of a test/optimization pass. When calling it, the entire

trading statistics and OnTester result are passed to the client terminal just like during the normal test/optimization completion.

- Added the new property for custom indicators #property

tester_everytick_calculate. It is used in the strategy tester and allows

for forced indicator calculation at each tick.

Tester

- Now, in case of a non-visual test/optimization, all used

indicators (standard and custom ones) are calculated only during a data

request. The exceptions are indicators containing the EventChartCustom function calls and applying the OnTimer

handler. Previously, all indicators were unconditionally calculated in

the strategy tester at each incoming tick (even from some other

instrument). The new feature significantly accelerates testing and

optimization.

To enable the forced indicator calculation at each tick, add the #property tester_everytick_calculate property for the program.

Indicators compiled using the previous compiler versions are calculated as before — at each tick.

- Fixed calculating the deposit currency accuracy when testing/optimizing and generating relevant reports.

- Optimized and accelerated the strategy tester operation.

- Fixed a few testing and optimization errors.

MetaEditor

- Fixed search for entire words. Now when searching, the

underscore is counted as a regular character, rather than a word

delimiter.

Updated documentation.

Terminal

- Added calculation of the price history of synthetic symbols for the entire available data depth.

The platform calculates the history of one-minute bars based on minute bars of instruments as applied in its formula. Previously, the history was only calculated for the last two months. A deeper history could be created upon an explicit request (when scrolling the chart to the left or calling Copy functions). Now, the history is calculated using all available data unconditionally.

Each symbol used in the synthetic formula can have price history of different depth. Synthetic history calculation is performed for the shortest available period. For example, the formula uses three financial instruments:

- EURUSD with the history down to 2009.01.01

- USDJPY with the history down to 2012.06.01

- EURJPY with the history down to 2014.06.01

In this case, the history of the synthetic symbol will be calculated for a period from 2014.06.01 to the present. 100 minutes will be additionally discarded from this date, to ensure the calculation integrity (if any minute bar is not available in history, a previous minute bar is used in the calculation).

If deep history of used symbols is available, the synthetic symbol history calculation can take quite a long time. To enable immediate synthetic symbol chart view, the history for the last two months is calculated first (similarly to calculations in previous versions). Calculation of an earlier history begins after that.

MQL5

- New property ACCOUNT_CURRENCY_DIGITS — the number of decimal places in the account deposit currency. Use the AccountInfoInteger function to get the property. You may use the property when calculating profit on your own, to normalize the values obtained.

- Fixed delay in the execution of Copy functions and i-functions during operations with the weekly timeframe.

- Fixed operation of the WebRequest function.

Tester

- Added ability to perform a single Expert Advisor test after downloading optimization results from a cache file.

- The new version features a faster initial download of price history by local agents.

Documentation has been updated.

Terminal

- Search for trading symbols by ISIN (International Securities

Identification Number) has been added in the Market Watch window. Now,

you can add symbols using three methods: by name, description and ISIN.

- Fixed user interface slowdown when changing a trading account password.

- Fixed occasional CPU load increase caused by the client terminal.

MQL5

- Fixed passing of custom HTTP headers in the WebRequest function.

- Fixed behavior of the Bars function in cases when the range beginning and end dates are the same. Now, if there is a bar, the function returns 1. In earlier versions, the function unconditionally returned 0.

Tester

- Fixed start of single testing in the visual mode after a forward optimization.

- Fixed sorting of optimization results. Now sorting takes into account passes with incorrect input parameters (INIT_INCORRECT_PARAMETERS) and those having no profit factor.

- Fixed recalculation of genetic optimization graph after changing the optimization criterion.

Documentation has been updated.

Terminal

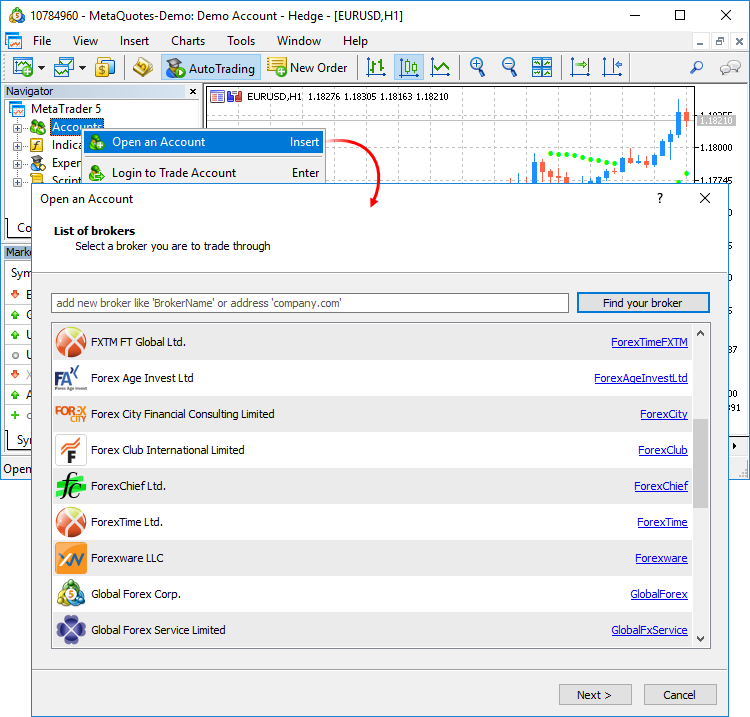

- The account opening dialog has been completely redesigned.

Now, you may select a broker from the list and then choose the desired

account type. This update has made the list of brokers more compact,

since now it only displays company names instead of showing all

available servers.

Company logos are additionally shown in the list to make the search easier and more efficient. If the desired broker is not shown in the list, type the company name or the server address in the search box and click "Find your broker".

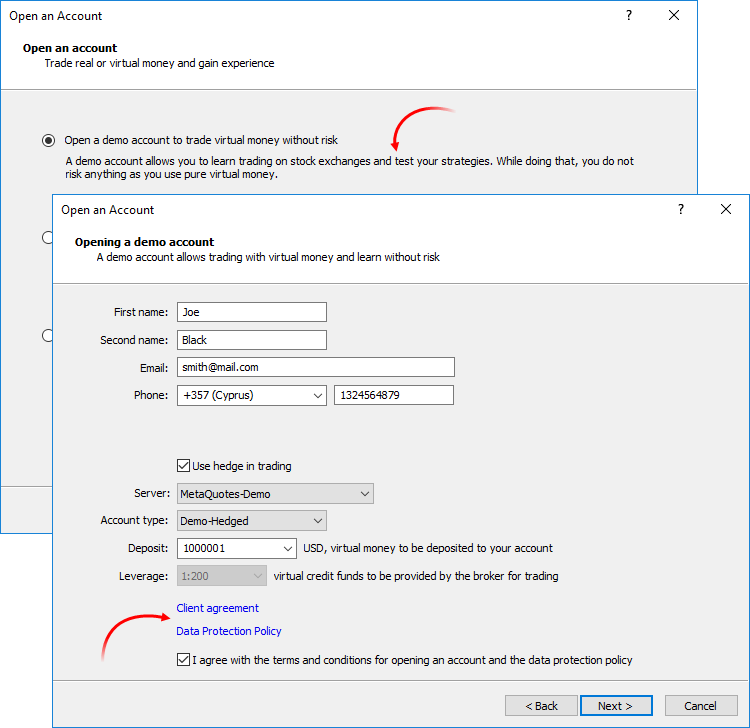

Descriptions of account types have been added to the dialog to help beginners choose the right account. Also, to align with the General Data Protection Regulation (GDPR), the updated dialog may contain links to brokers' agreements and data protection policies:

The possibilities for opening real accounts have been significantly expanded. The functionality for uploading ID and address confirmation documents, which was earlier presented in mobile terminals, is now available in the desktop version. Now, MiFID regulated brokers can request any required client identification data, including information on employment, income, trading experience, etc. The new functionality will help traders to open real accounts faster and easier, without unnecessary bureaucratic procedures.

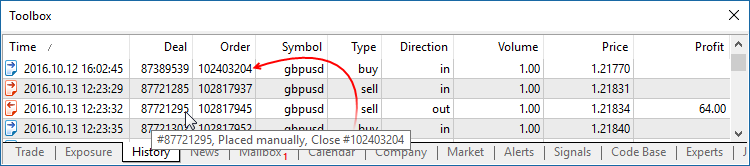

- The history of deals now displays the

values of Stop Loss and Take Profit. Stop Loss and Take Profit values

for entry and reversal deals are set in accordance with the Stop Loss

and Take Profit of orders, which initiated these deals. The Stop Loss

and Take Profit values of appropriate positions as of the time of

position closing are used for exit deals. The latter allows saving and

showing information about Stop Loss and Take Profit of a position as of

the moment of its closure. This information was not stored in earlier

versions, since positions disappear after closure, while the history of

positions in the terminal is generated based on deals.

- The history of positions now displays the values of Stop Loss and Take

Profit. Stop Loss and Take profit values of deals, which open and close

appropriate positions, are specified for such positions.

- Now, the current volume of pending orders is shown on the chart, instead of the initially requested volume.

- The updated terminal features optimized and faster rendering of the Market Depth feature in the extended mode with the enabled spread display.

- Processing of trade request execution results has been optimized. This optimizations leads to a much faster processing in some cases.

- Fixed error in Trailing Stop operation, which could occasionally lead to sending of several Stop Loss modification requests for the same position.

- Fixed setting of minimum and maximum volume, as well as volume step in custom symbol settings.

- Fixed error, due to which the "Fix Scale" option could be ignored, when applying a template to a symbol chart.

- Fixed occasional incorrect accumulation of tick history.

MQL5

- The speed of MQL5 applications has increased due to the additional

source code optimization during compilation. Recompile your programs in

the new MetaEditor version to make them run faster.Unfortunately, new programs will not be compatible with previous terminal versions due to this additional optimization. Programs compiled in MetaEditor version 1860 and later cannot be launched in terminal versions below 1860. Programs compiled in earlier MetaEditor versions can run on new terminals.

- New functions: iTime, iOpen, iHigh, iLow, iClose, iVolume, iBars,

iBarShift, iLowest, iHighest, iRealVolume, iTickVolume, iSpread. These

functions are similar to those used in MQL4. The functions provide for

an easier transfer of code of trading applications to the fifth

generation platform.

Earlier, most of tasks performed through these functions could be implemented using Copy* functions. However, users had to implement their own functions in order to find the High/Low values on the chart and to search for bars based on their time. Now, these tasks can be easily executed using iHighest, iLowest and iBarShift functions.

iTime

Returns the Open time of the bar (indicated by the 'shift' parameter) on the corresponding chart.datetime iTime( string symbol, // Symbol ENUM_TIMEFRAMES timeframe, // Period int shift // Shift );

iOpen

Returns the Open price of the bar (indicated by the 'shift' parameter) on the corresponding chart.double iOpen( string symbol, // Symbol ENUM_TIMEFRAMES timeframe, // Period int shift // Shift );

iHigh

Returns the High price of the bar (indicated by the 'shift' parameter) on the corresponding chart.double iHigh( string symbol, // Symbol ENUM_TIMEFRAMES timeframe, // Period int shift // Shift );

iLow

Returns the Low price of the bar (indicated by the 'shift' parameter) on the corresponding chart.double iLow( string symbol, // Symbol ENUM_TIMEFRAMES timeframe, // Period int shift // Shift );

iClose

Returns the Close price of the bar (indicated by the 'shift' parameter) on the corresponding chart.double iClose( string symbol, // Symbol ENUM_TIMEFRAMES timeframe, // Period int shift // Shift );

iVolume

Returns the tick volume of the bar (indicated by the 'shift' parameter) on the corresponding chart.long iVolume( string symbol, // Symbol ENUM_TIMEFRAMES timeframe, // Period int shift // Shift );

iBars

Returns the number of bars of a corresponding symbol and period, available in history.int iBars( string symbol, // Symbol ENUM_TIMEFRAMES timeframe // Period );

iBarShift

Search bar by time. The function returns the index of the bar corresponding to the specified time.int iBarShift( string symbol, // Symbol ENUM_TIMEFRAMES timeframe, // Period datetime time, // Time bool exact=false // Mode );

iLowest

Returns the index of the smallest value found on the corresponding chart (shift relative to the current bar).int iLowest( string symbol, // Symbol ENUM_TIMEFRAMES timeframe, // Period int type, // Timeseries identifier int count, // Number of elements int start // Index );

iHighest

Returns the index of the largest value found on the corresponding chart (shift relative to the current bar).int iHighest( string symbol, // Symbol ENUM_TIMEFRAMES timeframe, // Period int type, // Timeseries identifier int count, // Number of elements int start // Index );

iRealVolume

Returns the real volume of the bar (indicated by the 'shift' parameter) on the corresponding chart.long iRealVolume( string symbol, // Symbol ENUM_TIMEFRAMES timeframe, // Period int shift // Shift );

iTickVolume

Returns the tick volume of the bar (indicated by the 'shift' parameter) on the corresponding chart.long iTickVolume( string symbol, // Symbol ENUM_TIMEFRAMES timeframe, // Period int shift // Shift );

iSpread

Returns the spread value of the bar (indicated by the 'shift' parameter) on the corresponding chart.long iSpread( string symbol, // Symbol ENUM_TIMEFRAMES timeframe, // Period int shift // Shift );

- New TesterHideIndicators

function has been added. The function sets the show/hide mode for

indicators used in Expert Advisors. The function is intended for

managing the visibility of used indicators only during testing. Set to

true if you need to hide created indicators. Otherwise use false.

void TesterHideIndicators( bool hide // Flag );

- Added generation of the CHARTEVENT_CLICK event at a click on trade levels on the chart.

- Fixed and optimized operation of CopyTicks functions.

- Fixed value returned by the SymbolInfoDouble function for the SYMBOL_TRADE_LIQUIDITY_RATE property.

- Fixed copying of string arrays with overlapping memory.

- Fixed allocation of a string array in the FileReadArray array.

- Fixed errors in the MQL5 Standard Library.

Tester

- The system for working with the optimization cache has been updated.

The cache stores data about previously calculated optimization passes.

The strategy tester stores the data to enable resuming of optimization

after a pause and to avoid recalculation of already calculated test

passes.

Changes in the optimization cache storage format

In earlier versions, optimization cache was stored as one XML file. All Expert Advisor optimization passes with the specified testing settings were added to this file. Therefore, the same file stored results of optimizations with different input parameters.

Now, the optimization cache is stored as separate binary files for each set of optimized parameters. Strategy Tester operations involving the optimization cache have become significantly faster due to the new format and smaller file size. The acceleration can be especially noticeable when you resume a paused optimization pass.

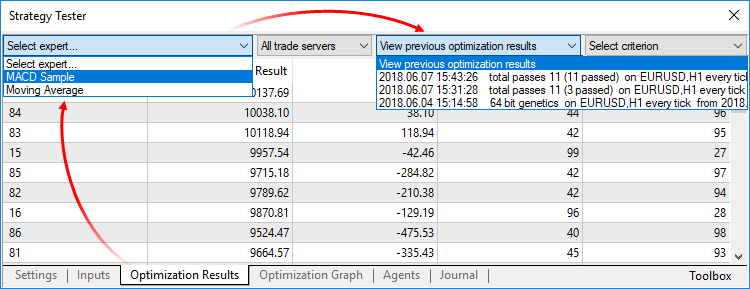

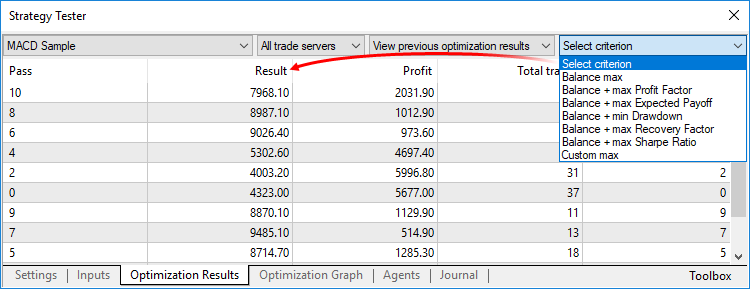

Viewing results of earlier optimizations

Now, the results of earlier optimizations can be viewed right in the Strategy Tester, so there is no need to analyze huge XML files using third-party software. Open the "Optimization results" tab, select an Expert Advisor and a file with the optimization cache:

The list contains all optimization cache files existing on the disk for the selected Expert Advisor. Optimization date, testing settings (symbol, timeframe, interval) and input parameters are shown for each file. You can additionally filter optimization results by the trade server, on which the results were obtained.

Recalculation of the optimization criterion on the fly

An optimization criterion is a certain variable parameter, the value of which determines the quality of a tested set of inputs. The higher the value of the optimization criterion, the better the testing result with the given set of parameters is considered to be.

Earlier, only one criterion selected before optimization start was calculated during optimization. Now, you can change the optimization criterion on the fly when viewing results, and the Strategy Tester will automatically recalculate all values.

Manual use of the optimization cache

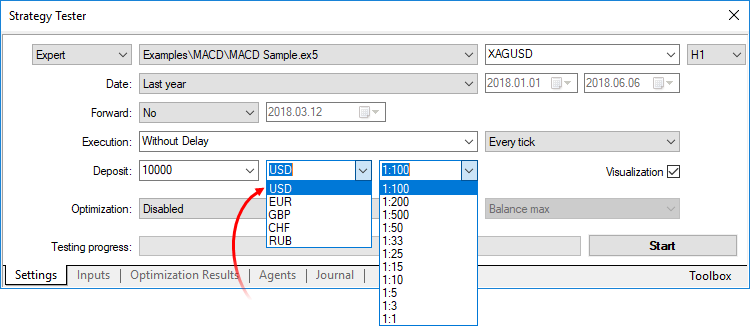

In earlier versions, optimization cache was stored as an XML file, which could be opened and analyzed using third-party software. Now it is stored in closed binary files. To get data in XML format, export them using the context menu of the "Optimization Results" tab. - Added possibility to manually set the deposit currency and leverage for

testing and optimization. In earlier versions, the currency was set in

accordance with the connected account. Therefore, one had to switch to

other accounts in order to change the currency. The leverage size could

only be selected from a predefined list, now any value can be specified.

Please note that cross rates for converting profit and margin to the specified deposit currency must be available on the account, to ensure proper testing.

- Removed ban on the use of OpenCL

in testing agents. Earlier, OpenCL devices were only allowed when

testing on local agents. Now, agents are allowed to use all available

OpenCL devices (such as processor, video card) when working in the local

network and in the MQL5 Cloud Network.

MetaEditor

- Optimized and accelerated work with the MQL5 Storage.

- Fixed resuming of debugging process after a pause in the MQH file.

- Fixed source code highlighting in the editor.

- Fixed navigation through search results.

- Fixed mass text replace function. In some cases, only the first occurrence was replaced instead of all of them.

Documentation has been updated.

Terminal

- Fixed an error that caused the terminal and MetaEditor to block Windows shutdown and reboot.

- Fixed the chart shift when applying a template.

MQL5

- Fixed errors that slowed down compilation in some conditions.

Fixed errors reported in crash logs.

MetaTrader 5 build 1745 will be the last platform version supporting Microsoft Windows XP/2003/Vista.

A few months ago, we announced end of support for older versions of operating systems.

Windows 2003, Windows Vista and especially Microsoft Windows XP are

outdated operating systems. Microsoft ended support for Windows XP three

years ago, because potential hardware capabilities could no longer be

realized on this system due to technical limitations.

MetaTrader 5 build 1745 and older versions will continue to work on the above

operating systems, but will no longer receive updates. Platform

installers will not run on these operating systems.

The minimum

required operating system version for running MetaTrader 5 is Windows 7.

However, we strongly recommend using the 64-bit version of Windows 10.

Terminal

-

The /auto key has been added to the installer, allowing to install the

program in automated mode without additional actions required from the

user. When the installer is launched with this key, installation

settings will not be shown to the user, and the terminal will be

installed at the standard path, with the standard Start menu folder name

for the program. Example of such launch: C:\mt5setup.exe /auto

- Fixed installer operation in cases when the user does not have appropriate operating system permissions.

-

Fixed excessive consumption of CPU resources when no actions are

performed in the terminal (when there are no open charts and no actions

are performed by the user).

- The new version features automatic compression of *.log files at the file system level. The new functionality allows reducing the amount of disk space used by logs.

-

The amount of cache during single test runs has been increased. This

provides faster testing in 64-bit operating systems.

Tester

- Fixed optimization of trading robots using the MQL5 Cloud Network. Issues could arise with products purchased from the MetaTrader Market.

- Fixed calculation of spreads for bars generated in the "Every Tick" testing mode.

- Fixed selection of OpenCL devices in the strategy tester. Now, the visual tester is allowed to access all available OpenCL devices.

- The new version features automatic compression of *.log files at the file system level. The new functionality allows reducing the amount of disk space used by logs.

MQL5

- Fixed deletion of bars of a custom symbol using the CustomRatesDelete method.

Updated documentation.

End of Support for Older Terminal Versions!

Support for older versions of desktop and mobile terminals will end upon the release of the new platform version:

- Client Terminal: versions below 730, November 23, 2012

- Mobile Terminal for iPhone: versions below 1171, November 11, 2015

- Mobile Terminal for Android: versions below 1334, August 5, 2016

Unsupported terminal builds will not be able to connect to new server

versions. We strongly recommend that you update your terminals in

advance.

MQL5 Storage Operation Protocol Changes

To support new shared projects, we have updated the protocol of operation with the MQL5 Storage. Therefore, you will need to perform a checkout of all data from the storage after the platform update. Data stored at the MQL5 Storage will not be lost or affected during the update.

Before updating the platform to the new version, we recommend that you perform the Commit operation to send all local changes to the MQL5 Storage.

Terminal

Now, the trading platform allows creating synthetic financial instruments, i.e. symbols based on one or more existing instruments. The user should set the formula for calculating quotes, after which the platform will generate ticks of the synthetic instrument in real time, and also will create its minute history.

How It Works

- You create a synthetic instrument and set the formula for price calculation.

- The platform calculates ticks at a frequency of 10 times per second, provided that the price of at least one of the instruments used in the formula has changed.

- The platform also calculates the history of one-minute bars (for the last two months) based on minute bars of instruments used in its formula. All new bars (current and subsequent ones) are built in

real time based on the generated ticks of the synthetic instrument.

For example, you can create an instrument showing the dollar index (USDX). It uses the below formula:

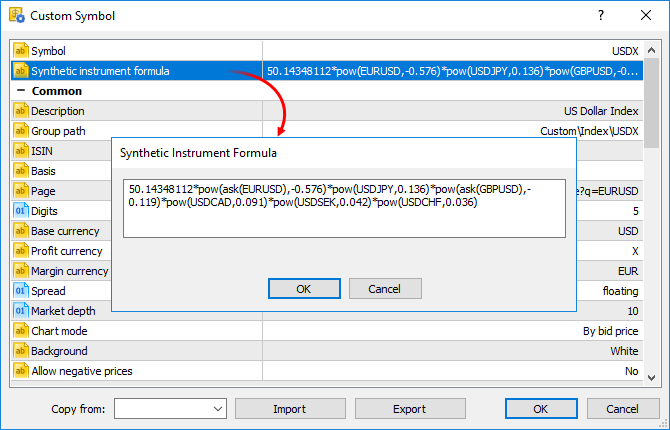

50.14348112 * pow(ask(EURUSD),-0.576) * pow(USDJPY,0.136) * pow(ask(GBPUSD),-0.119) * pow(USDCAD,0.091) * pow(USDSEK,0.042) * pow(USDCHF,0.036)

Note: the USDEUR and USDGBP pairs are used in the source dollar index formula. Since only reverse pairs are available in the platform, a negative power and Ask instead of Bid are used in the synthetic symbol formula.

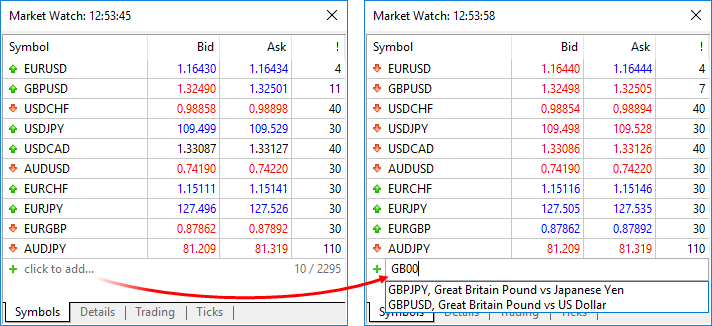

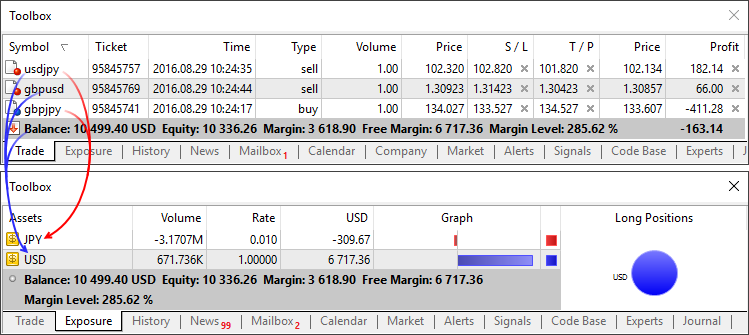

The platform will calculate in real time the price of the new instrument based on the quotes of the other six symbols provided by your broker. The price changes will be visualized in the Market Watch window and on the chart:

Create a new custom symbol, open its specification and enter the formula:

For convenience, the formula editor shows a list of possible options as you type the names of symbols and functions.

Calculation of ticks and one-minute bars of a synthetic instrument starts when this instrument is added to the Market Watch. Also, all symbols required for the synthetic price calculation are automatically added to the Market Watch. An entry about the calculation start will be added to the platform journal: Synthetic Symbol USDX: processing started.

- Calculation of a synthetic instrument stops after it is removed from the Market Watch.

- Symbols that are currently used for calculating synthetic symbol prices cannot be hidden from the Market Watch.

Real-Time Calculation of Quotes

Every 100 ms (i.e. ten times per second) the prices of symbols used in calculation are checked. If at least one of them has changed, the price of the synthetic symbol is calculated and a new tick is generated. Calculation is performed in parallel in three threads for Bid, Ask and Last prices. For example, if the calculation formula is EURUSD*GBPUSD, the price of the synthetic symbol will be calculated as follows:

- Bid = bid(EURUSD)*bid(GBPUSD)

- Ask = ask(EURUSD)*ask(GBPUSD)

- Last = last(EURUSD)*last(GBPUSD)

The availability of changes is checked separately for each price. For example, if only the Bid price of a source instrument has changed, only the appropriate price of a synthetic instrument will be calculated.

Creating a History of Minute Bars

In addition to collecting ticks in real time, the platform creates a minute history of the synthetic instrument. It enables traders to view synthetic symbol charts similar to normal ones, as well as to conduct technical analysis using objects and indicators.

When a trader adds a synthetic instrument to the Market Watch, the platform checks whether its calculated minute history exists. If it does not exist, the history for the last 60 days will be created, which includes about 50,000 bars. If a lower value is specified in the 'Max. bars in chart' parameter in platform settings, the appropriate restriction will apply.

If some of bars within this period have already been create, the platform will additionally generate new bars. A deeper history is created if the user tries to view an older time period on the chart (by scrolling it back or accessing it from an MQL5 program).

The history of one-minute bars of a synthetic instrument is calculated based one one-minute bars (not ticks) of instruments used in its formula. For example, to calculate the Open price of a 1-minute bar of a synthetic symbol, the platform uses the Open prices of symbols used in its formula. High, Low and Close prices are calculated in a similar way.

If the required bar is not available for any of the instruments, the platform will use the Close price of the previous bar. For example, three instruments are used: EURUSD, USDJPY and GBPUSD. If in the calculation of a bar corresponding to 12:00 the required bar of USDJPY is not available, the following prices will be used for calculation:

- Open: EURUSD Open 12:00, USDJPY Close 11:59, GBPUSD Open 12:00

- High: EURUSD High 12:00, USDJPY Close 11:59, GBPUSD High 12:00

- Low: EURUSD Low 12:00, USDJPY Close 11:59, GBPUSD Low 12:00

- Close: EURUSD Close 12:00, USDJPY Close 11:59, GBPUSD Close 12:00

If the minute bar is not available for all of the instruments used in the formula, the appropriate minute bar of the synthetic instrument will not be calculated.

Drawing New Minute Bars

All new bars (current and subsequent ones) of the synthetic instrument are created based on generated ticks. The price used for building the bars depends on the value of the Chart Mode parameter in the specification:

What Operations Can Be Used in the Symbol Formula

Price data and some properties of existing symbols provided by the broker can be used for calculating synthetic prices. Specify the following:

- Symbol name — depending on the synthetic price to be calculated, the Bid, Ask or Last of the specified instrument will be used. For example, if EURUSD*GBPUSD is specified, Bid is calculated as bid(EURUSD)*bid(GBPUSD), and Ask = ask(EURUSD)*ask(GBPUSD).

- bid(symbol name) — the bid price of the specified symbol will be forcedly used for calculating the Bid price of the synthetic instrument. This option is similar to the previous one (where the price type is not specified).

- ask(symbol name) — the Ask price of the specified symbol will be used for calculating the Bid price of the synthetic instrument. Bid price of the specified instrument will be used for calculating Ask. The Last price of the specified symbol will be used for calculating Last. If ask(EURUSD)*GBPUSD is specified, the following calculation will be used:

- Вid = ask(EURUSD)*bid(GBPUSD)

- Ask = bid(EURUSD)*ask(GBPUSD)

- Last = last(EURUSD)*last(GBPUSD)

- last(symbol name) — the Last price of the specified symbol will be used in the calculation of all prices of the synthetic instrument (Bid, Ask and Last). If last(EURUSD)*GBPUSD is specified, the following calculation will be used:

- Вid = last(EURUSD)*bid(GBPUSD)

- Ask = last(EURUSD)*ask(GBPUSD)

- Last = last(EURUSD)*last(GBPUSD)

- volume(symbol name) — the tick volume of the specified instrument will be used in the formula. Make sure that volume information is provided by the broker for this symbol.

- point(symbol name) — the minimum price change of the specified instrument will be used in calculations.

- digits(symbol name) — the number of decimal places in the specified symbol price will be used in the formula.

If a symbol has a complex name (contains hyphens, dots, etc.), it must be written in quotation marks. Example: "RTS-6.17".

The following arithmetic operations can be used in the formula: addition (+), subtraction (-), multiplication (*), devision (/) and remainder of division (%). For example, EURUSD+GBPUSD means that the price is calculated as the sum of EURUSD and GBPUSD prices. Also you can use the unary minus to change the sign, for example: -10*EURUSD.

Mind the calculation priority of arithmetic operations:

- The operations of multiplication, division and remainder are performed first; then addition and subtraction operations are performed.

- The operations are performed from left to right. If the formula uses several operations that have the same priority (for example, multiplication and division), the operation on the left will be performed first.

- You can use brackets ( and ) to change the priority of operations. Operations in brackets have the highest priority in the calculation. The left-to-right principle also applies for them: operations in brackets on the left are calculated first.

You can use constants in the formula:

- Numerical (integer and float). Example: EURUSD*2+GBPUSD*0.7.

- Symbol properties _Digits and _Point. They add to the formula appropriate properties of the custom symbol from the specification. _Digits means the number of decimal places in the instrument price; _Point means the smallest change in the symbol price.

You can also use in the formula all mathematical functions supported in MQL5, except for MathSrand, MathRand and MathIsValidNumber: Only short names are used for all functions, such as fabs(), acos(), asin() etc.

- A new option has been implemented, allowing to add quotes of custom instruments in real time. Now, it is possible to develop an MQL5 Expert Advisor that would be feeding quotes of the

specified custom symbol. The CustomTicksAdd function is used for that.

int CustomTicksAdd( const string symbol, // Symbol name const MqlTick& ticks[] // The array with tick data that should be applied to the custom symbol );

The CustomTicksAdd function allows feeding quotes as if these quotes were received from a broker's server. Data is sent to the Market Watch window instead of being directly written to the tick database. Then, the terminal saves ticks from the Market Watch to the database. If a large volume of data is passed in one call, the function behavior changes, in order to save resources. If more than 256 ticks are transmitted, data is divided into two parts. A larger part is recorded directly to the tick database (similar to CustomTicksReplace). The second part consisting of the last 128 ticks is sent to the Market Watch, from where the terminal saves the ticks to a database.

- The Market Watch window now additionally features the High and Low prices. These columns are hidden by default. They can be enabled using the context menu:

If a symbol chart is constructed using Bid prices (as per specification settings), Bid High and Bid Low prices are shown for this symbol. If a symbol chart is constructed using Last prices, Last High and Last Low prices are shown for this symbol.

If Market Watch contains at least one symbol whose chart is drawn based on Last prices, the Last column is automatically enabled in addition to High/Low.

- Now it is possible to edit the tick history of custom financial instruments. Click 'Symbols' in the Market Watch context menu, select a custom symbol and request the required data interval in the

Ticks tab.

- Double-tap to change the value.

- Use the context menu to add or delete entries.

- If you need to delete multiple bars/ticks at once, select them with the mouse, holding down Shift or Ctrl+Shift.

For convenience, modified entries are highlighted as follows:

- Green background indicates a modified entry

- Gray background means a deleted entry

- Yellow background shows an added entry

To save the changes, click "Apply Changes" at the bottom of the window.

- Added display of preliminary accounts in the Navigator tree.

Traders can send a request to a broker to open a real account straight from desktop terminals. The user needs to fill in a simple request form with contact details. A special preliminary account is created for the trader after that. Then, the broker contacts the trader to formalize relations and turn the real account from the preliminary one.

- Added display of time in millisecond in the Quotes window.

- Scanning of available servers in the new account opening dialog has become faster.

- Fixed display of the Trendline graphics object with the Ray Left and Ray Right options enabled.

- Optimized operation with a large amount of internal emails (hundreds of thousands).

- Optimized terminal operation with a large amount of trading instruments (50,000 or more).

- Added optimization of the tick history of custom financial instruments executed after editing history.

MetaEditor

Full-featured projects are now available in MetaEditor. The program development process has become more convenient.

Now the main MQ5 program file does not appear as the project. The project is a separate "MQPROJ" file, which stores program settings, compilation parameters and information about all used files. Main project settings can be accessed from a separate dialog box, so there is no need to specify them in the source code via #property now.

A separate tab in the Navigator is provided for work convenience within the project. All files, such as include, resource, header and other files are arranged into categories on this tab. All files are automatically added to the project navigator. For example, if you include a new MQH file, it will automatically appear in the "Dependencies" section of the navigator.

Support for new projects has also been implemented in the updated MQL5 Storage online repository. Now, it has become much more convenient to develop large projects through collaboration with other members of the MQL5.community.

New Shared Projects section is provided for group projects. A project created in this section is immediately sent to the storage: you can grant permissions to other users and start collaboration right away.

When you compile a project in Shared Projects, an executable EX5 file is automatically copied to the local Experts, Indicators or Scripts directory depending on the program type. You can easily launch the program on a chart without having to copy files manually.

What's New in the MQL5 Storage Operation

To implement support for new shared projects, we have modified the protocol of operation with the MQL5 Storage. Therefore, you will need to perform a checkout of all data from the storage after the platform update. Data stored at the MQL5 storage will not be lost or affected during the update.

Before updating the platform to the new version, we recommend that you perform the Commit operation to send all local changes to the MQL5 Storage.

The 'Checkout from Storage' command is unavailable now. Instead, the 'Activate MQL5 Storage' and 'Update from Storage' commands are used to receive data: